Should I Use My 401(k) to Buy an Annuity?

Many employer 401 (k) plans offer an option to purchase an annuity. But should you? This isn’t a decision to be made lightly.

Annuities can be overly complex and expensive products. An annuity can be a useful tool in certain situations, but there’s more to the situation than many people realize. You really need to think through your long-term retirement income and tax situation.

Table of Contents

What It Actually Means to Use Your 401(k) for an Annuity

You may have seen the option to buy an annuity or “annuitize” your employer plan like a 401k. This can seem simple, but it’s often more complicated than you might realize. And you might not have many options to choose from.

Ultimately, purchasing an annuity starts with your employer and their 401k provider. You are limited to the options inside your employer plan, if any. But first, let’s back up and talk about whether you need an annuity at all.

Retirement Income Needs Come First

We always want you to consider your goals and needs first, then select the right tool for the job. In reality, you’ll probably have some guaranteed retirement income through Social Security. In addition to your retirement savings, you might have other streams of retirement income, like rental properties or a pension.

Do you have over $1 Million in retirement assets? Check these strategies to tackle High Net Worth Investor (HNWI) concerns.

Understanding How Annuities Fit Inside a 401(K) or IRA Rollover

Before the original SECURE Act and SECURE Act 2.0, annuities weren’t offered inside 401ks. There were similar plans, like the Federal Thrift Savings Plan (TSP), which offered annuities, but not your average employer plan. Now, you can use some or all of your 401k to purchase an annuity inside the plan.

Before the SECURE Act, you’d select the annuity option from the available providers and then “roll” the selected amount into the annuity contract. This would create a qualified annuity held outside your 401k. Payments from the annuity would be taxable upon receipt, just like distributions.

Post SECURE Act Options

Now, you may have the option to purchase an annuity directly within your employer plan. This allows you to have everything held within the 401k. In practice, it’s just skipping the step of rolling your 401k out to an IRA first.

Rolling To an IRA For Annuity Purchase

You still have the option to complete a rollover to an IRA. Then you can either invest in your own investment portfolio or purchase an annuity. This is still a common method for purchasing annuities.

Types of Annuities Commonly Used

There are several types of annuities, including fixed, indexed, and income annuities. Once again, you’ll need to understand how each type of annuity fits into your overall retirement plan. There are multiple “flavors” of each type of annuity.

Also, each insurance company will have its own selection of products, features, costs, and fees. The type of annuity you choose, if any, changes the structure of your retirement income. Be sure to read all the fine print and understand how each rider or income option affects the other options in the annuity.

Check the Fine Print

Annuity contracts can often be somewhat circular in nature. If you’re not careful, you can end up in an endless, confusing loop of if-this, then-that statements inside the contract. If you can’t easily understand how much you’re paying, how your payments are calculated, and how life changes affect the contract, reach out to a financial planner for assistance.

When Using a 401(k) for an Annuity Makes Sense

If it sounds like we’re cautious on annuities, there’s a reason. Most people don’t need an annuity to meet their retirement needs. However, there are large financial incentives for those who sell annuities (we don’t sell annuities).

If you can cover your essential expenses with Security and regular withdrawals from your retirement accounts, you probably don’t need an annuity. However, if you’re stressed about outliving your money or don’t have Social Security or other pension income, it might make sense.

In reality, an annuity is simply insurance you can purchase to protect you from outliving your money. You pay a fee to transfer your longevity risks to an insurance company.

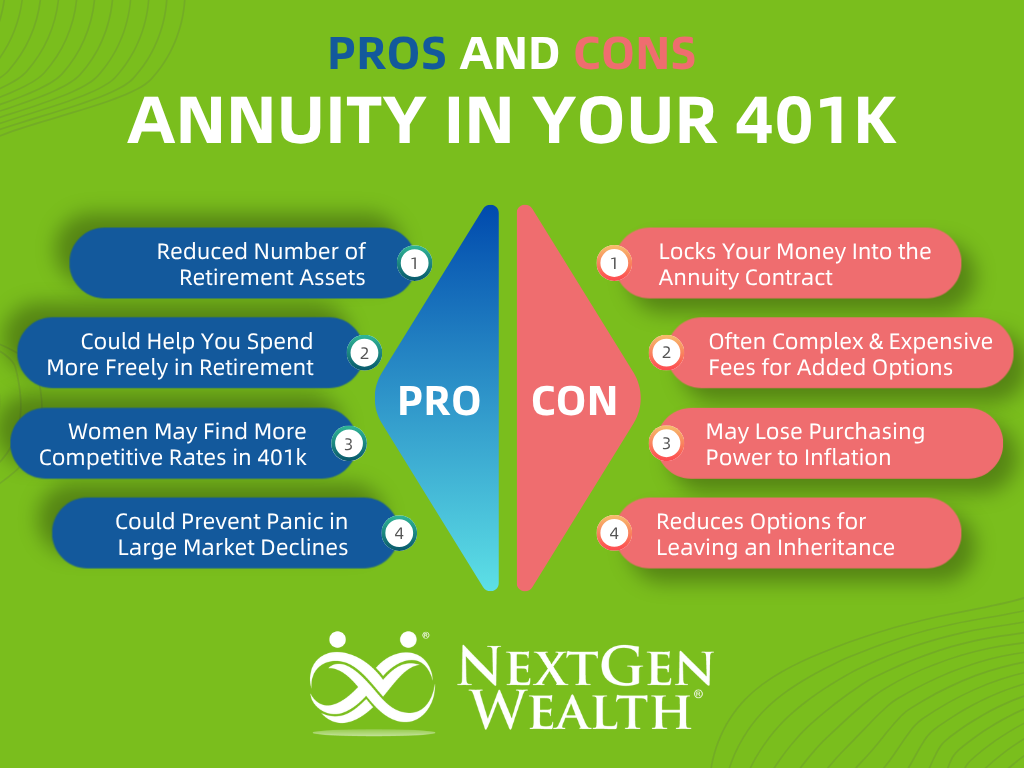

Simplification of Retirement Assets

Annuities are often marketed as an option to simplify retirement income. This can be appealing for clients who don’t want to manage investments. However, annuities are anything but simple.

Annuities are complex products with many pages of legally binding contractual agreements. They’re easy to buy, but difficult or expensive to get out of. You’ll be subject to a surrender charge if you try to end your contract early.

It sounds simple to trade your money for a stream of monthly payments, but the mechanics of how it happens aren’t always very straightforward.

Behavioral Benefits

Another potential benefit of an annuity is its behavioral effect on spending in retirement. Retirees have shown they’re more willing to spend more from guaranteed, lifetime sources than their savings. There may also be some benefits to reducing panic during market volatility.

Potential Cost Savings for Employer Plans

If you’re planning to purchase an annuity, there may be circumstances in which your costs could be lower. Employers may be able to get preferential pricing by pooling assets together versus an individual on their own.

It might also be possible for women to get better annuity pricing. Since employer plans must be gender-neutral in pricing, female employees may get slightly better annuity prices than they could on the open market. Differences will vary by annuity type, retirement date, and insurance carrier.

When It Might Not Be the Right Move

For each potential benefit of purchasing an annuity, there are potential drawbacks. These are long-term and costly decisions, so make sure you know what you’re getting into.

Loss of Liquidity and Flexibility

One major concern with annuities is locking up your money. Once you buy an annuity, you’re usually locked in for a certain number of years unless you pay the surrender charges. Even if you complete a 1035 exchange, you’re still not off the hook for surrender charges.

Fees, Complexity, and Surrender Charges

Insurance companies always charge a fee for the service they provide. In the case of annuities, they’re providing a contracted amount of income over a specified period (normally your life expectancy). You may have other add-on features called riders, which add to costs and complexity as well.

Surrender Charges

As we mentioned earlier, annuities are generally sold on commission, so the insurance company incurs a cost immediately upon purchase. Surrender charges ensure the issuing company recovers its money from paying the insurance agent who sold you the policy.

Insurance companies aren’t going to offer a deal if there’s a high chance of losing money. Just like casinos, the house always wins. Insurance companies employ teams of lawyers and actuaries to make certain they’ll remain profitable and protected from losses.

Inflation Risk and Purchasing Power Concerns

Many annuities offer a fixed payment during the payout period. This might be good to start, but inflation will increase your living expenses over time. You might be better served with a diversified portfolio to keep some of your money growing.

Keeping your retirement savings invested with a tailored withdrawal strategy may be more effective. You can still increase your retirement savings, implement tax-saving strategies, and maintain flexibility.

Leaving an Inheritance

In most cases, when you pass away, your annuity payments stop. You might have the option for a death benefit, but only if you pay for it. Every rider on your annuity costs you something.

Annuities aren’t a great option if you want to leave something behind for your children or grandchildren. You need to do what’s best for you, but it’s nice knowing the ones you leave behind will have some options.

The Bottom Line on Annuities

Most retirees don’t need an annuity to meet their retirement goals. If you have a reasonable amount of retirement savings in a diversified portfolio and Social Security, you’ll probably be okay. We always recommend considering your long-term spending needs and goals, then selecting investments and tools to meet them.

How NextGen Wealth Can Help

During our COLLAB™ Financial Planning Process, we help clients uncover their goals and understand their assets. Then, we build a cohesive financial plan to make the most of your retirement. Contact us today to schedule your no-obligation financial assessment and see if we’re a good fit to work together.

This article was written by

This article was written by